The relationship between power generation and property value has never been more intimate. As artificial intelligence drives an unprecedented surge in electricity demand, a new generation of nuclear technology is quietly rewriting the rulebook for real estate development across continents. Small modular reactors, once a theoretical concept confined to engineering journals, are now forcing investors, developers, and municipalities to reconsider where—and how—they build.

The New Nuclear Renaissance

Walking through the exhibition halls at last year’s World Nuclear Symposium in London, one couldn’t help but notice the shift in conversation. Gone were the days when nuclear energy meant solely massive cooling towers and decades-long construction timelines. In their place, sleek models of compact reactors sat alongside digital renderings of industrial parks powered by what insiders call SMRs—small modular reactors.

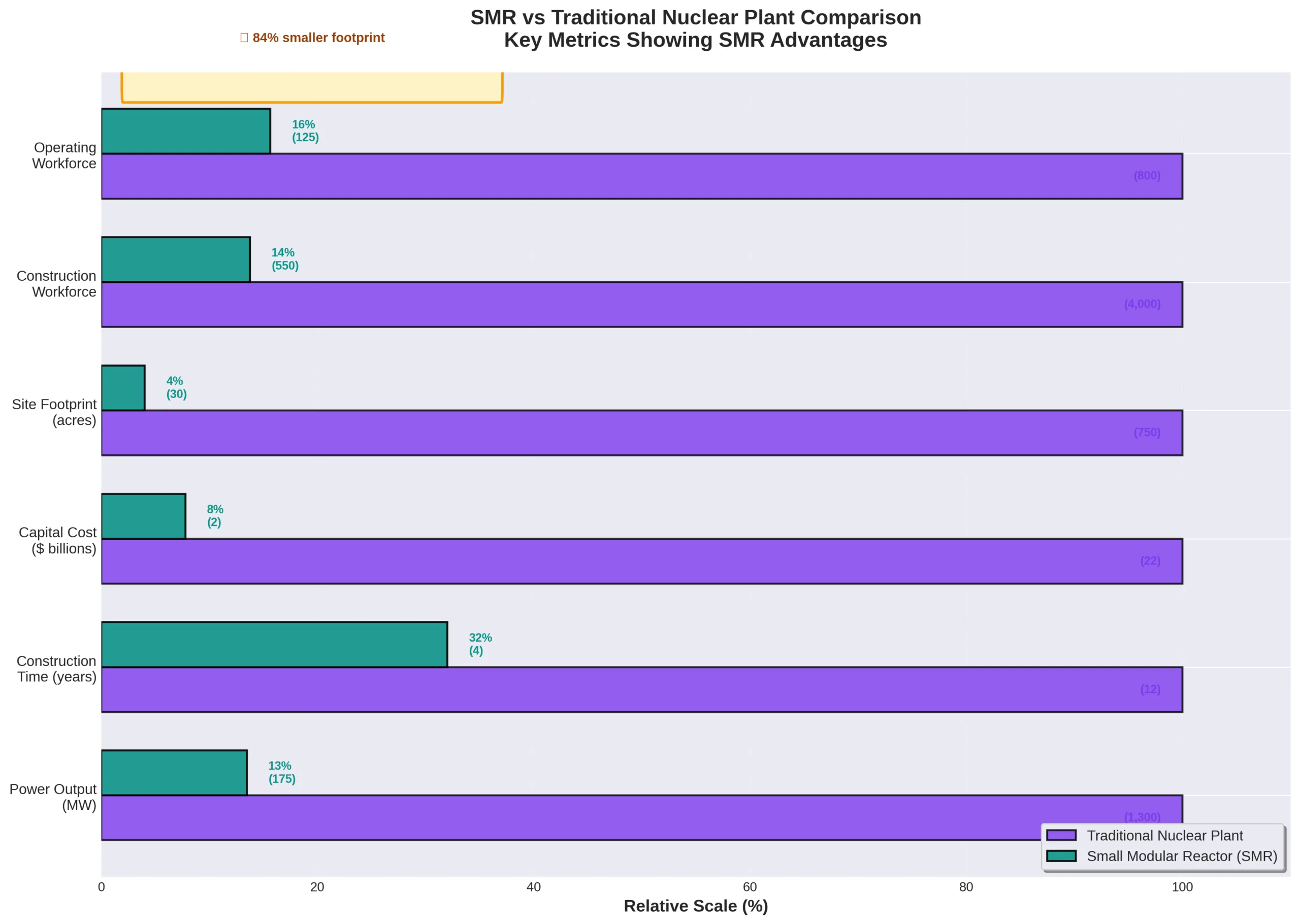

These aren’t your grandfather’s nuclear plants. Where traditional reactors can take fifteen years to construct and cost upwards of $15 billion, SMRs promise factory assembly, truck delivery, and price tags under $1 billion. The implications for real estate are profound and immediate.

“We’re seeing inquiries from institutional investors who previously wouldn’t have considered proximity to power infrastructure as a primary criterion,” says Margaret Chen, a partner at a London-based infrastructure investment firm specializing in energy transition projects. “Now it’s often their opening question: What’s the power situation?”

A Technology Landscape in Flux

The nuclear renaissance isn’t monolithic. Three distinct technological approaches are competing for dominance, each with different implications for land use and site selection.

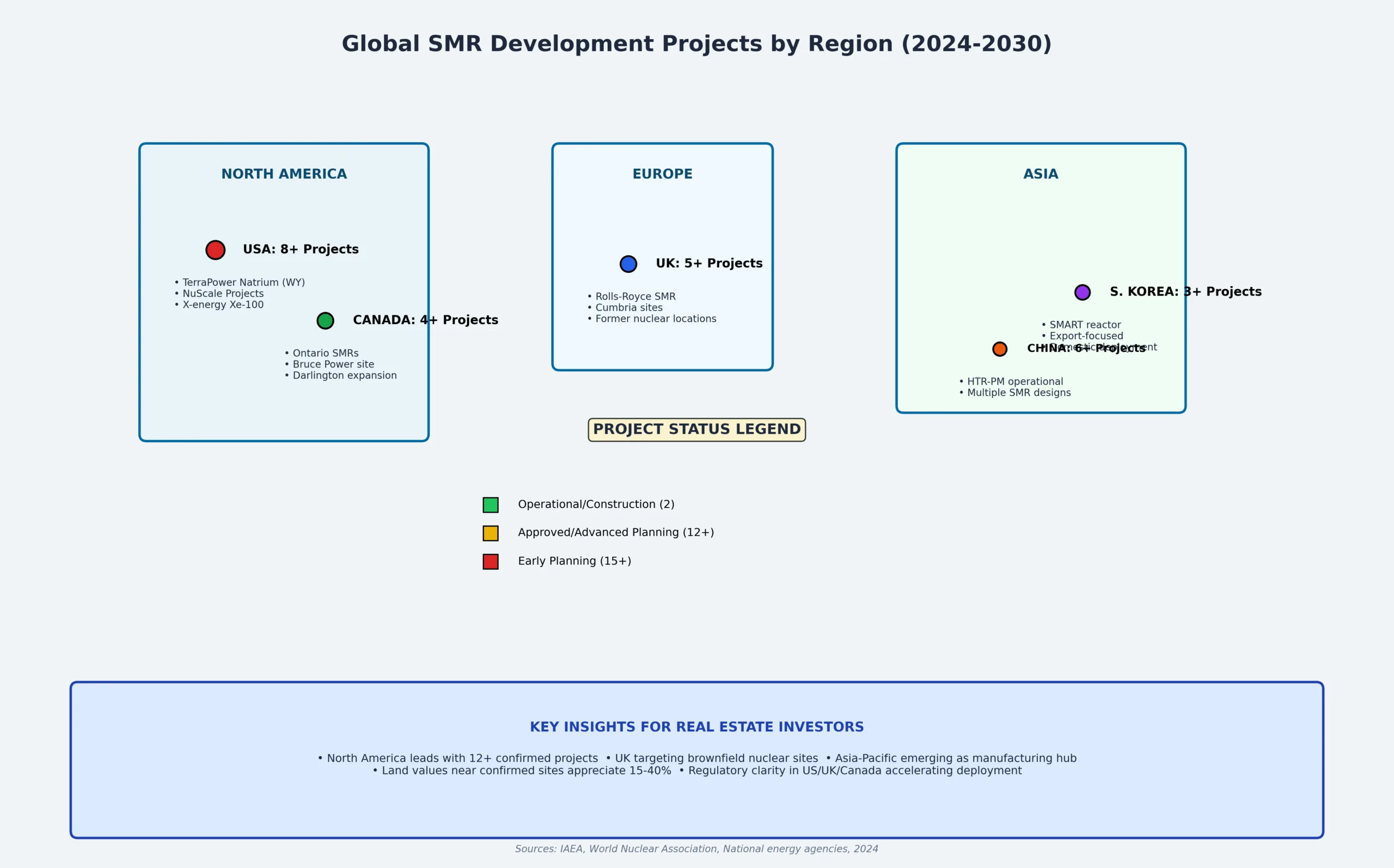

Small Modular Reactors (SMRs) represent the most commercially advanced category. Companies like NuScale Power in the United States and Rolls-Royce SMR in the United Kingdom are developing units that generate between 50 and 300 megawatts—enough to power a mid-sized data center campus or small city. Their modular design allows for factory fabrication and relatively rapid deployment. The Canadian province of Ontario recently committed to building SMRs at existing nuclear sites, recognizing that brownfield development minimizes community opposition and accelerates regulatory approval.

High-Temperature Gas-Cooled Reactors (HTGRs) offer something different: process heat. While SMRs primarily generate electricity, HTGRs can provide the extreme temperatures needed for industrial processes like hydrogen production or chemical manufacturing. China has taken the lead here, successfully connecting its HTR-PM demonstration reactor to the grid in 2021. For real estate developers, this technology signals a potential return of heavy industry to locations previously written off as economically unviable due to energy costs.

Sodium-Cooled Fast Reactors complete the trifecta, promising enhanced safety profiles and the ability to consume nuclear waste as fuel. The U.S. Department of Energy has backed TerraPower’s Natrium reactor demonstration project in Wyoming, deliberately choosing a former coal plant site—a pattern that’s becoming increasingly common and reshaping the economic geography of aging industrial regions.

Each technology creates different footprints, different buffer zones, and different ancillary infrastructure needs. For those mapping real estate opportunities, understanding these distinctions matters enormously.

National Strategies, Regional Impacts

The global race toward advanced nuclear deployment reflects divergent national priorities, regulatory environments, and energy security concerns. These differences are creating distinct investment landscapes.

The United States is pursuing what might be called a “let markets decide” approach. The Nuclear Regulatory Commission has established new certification pathways for advanced reactors, but deployment depends largely on private sector initiatives. Tech giants like Microsoft and Amazon have announced power purchase agreements for SMR electricity specifically to supply their data center operations. This corporate-led demand is concentrating potential development in regions with existing grid infrastructure, favorable regulations, and political support—notably the Southeast and Mountain West.

Virginia, already home to the world’s largest concentration of data centers in Loudoun County, has seen land values in adjacent counties appreciate by double-digit percentages as energy-hungry facilities scout for expansion options. The calculus has changed: it’s no longer just about fiber optic connectivity, but about long-term power availability.

The United Kingdom is taking a more dirigiste path. The government has designated sites for both large-scale and small modular reactor development, with Rolls-Royce SMR targeting deployment by the early 2030s. British energy policy explicitly links nuclear expansion to industrial strategy, viewing reliable baseload power as essential for maintaining manufacturing competitiveness. For property investors, this creates a degree of predictability: brownfield sites near existing nuclear installations and former industrial centers are receiving renewed attention.

Cumbria, home to the Sellafield nuclear site, is experiencing an unexpected property renaissance. Commercial real estate that languished for decades now attracts interest from logistics companies, technical service providers, and housing developers anticipating an influx of specialized workers.

Canada offers perhaps the most instructive case study in coordinated energy and economic development planning. Ontario Power Generation’s commitment to build multiple SMRs at existing nuclear sites represents not just energy policy but regional economic development strategy. The Crown corporation has explicitly framed these projects as economic anchors for communities facing transition as coal plants retire.

The town of Darlington, Ontario, exemplifies this approach. Local officials speak candidly about using confirmed SMR deployment as leverage to attract advanced manufacturers who need reliable, carbon-free power. Residential developers are already responding, with new subdivisions marketed explicitly to technical professionals expected to staff both the reactors and the industries they’ll power.

South Korea demonstrates how government-industry coordination can accelerate deployment. With a mature domestic nuclear industry and aggressive decarbonization targets, Korea is simultaneously developing SMR technology for domestic deployment and export. Korean firms view SMRs as integrated packages—reactor, associated infrastructure, and operational expertise—suitable for wholesale export to Southeast Asian nations.

For real estate professionals watching Korean developments, the key insight involves supply chain geography. As component manufacturing scales up, industrial parks near production facilities are attracting warehouse and logistics operations positioning themselves to serve both domestic and international markets.

The Real Estate Calculus

Energy infrastructure has always influenced property development, but the relationship was typically indirect: industrial facilities needed power, so they located where power was cheap. The SMR era inverts this logic in crucial ways.

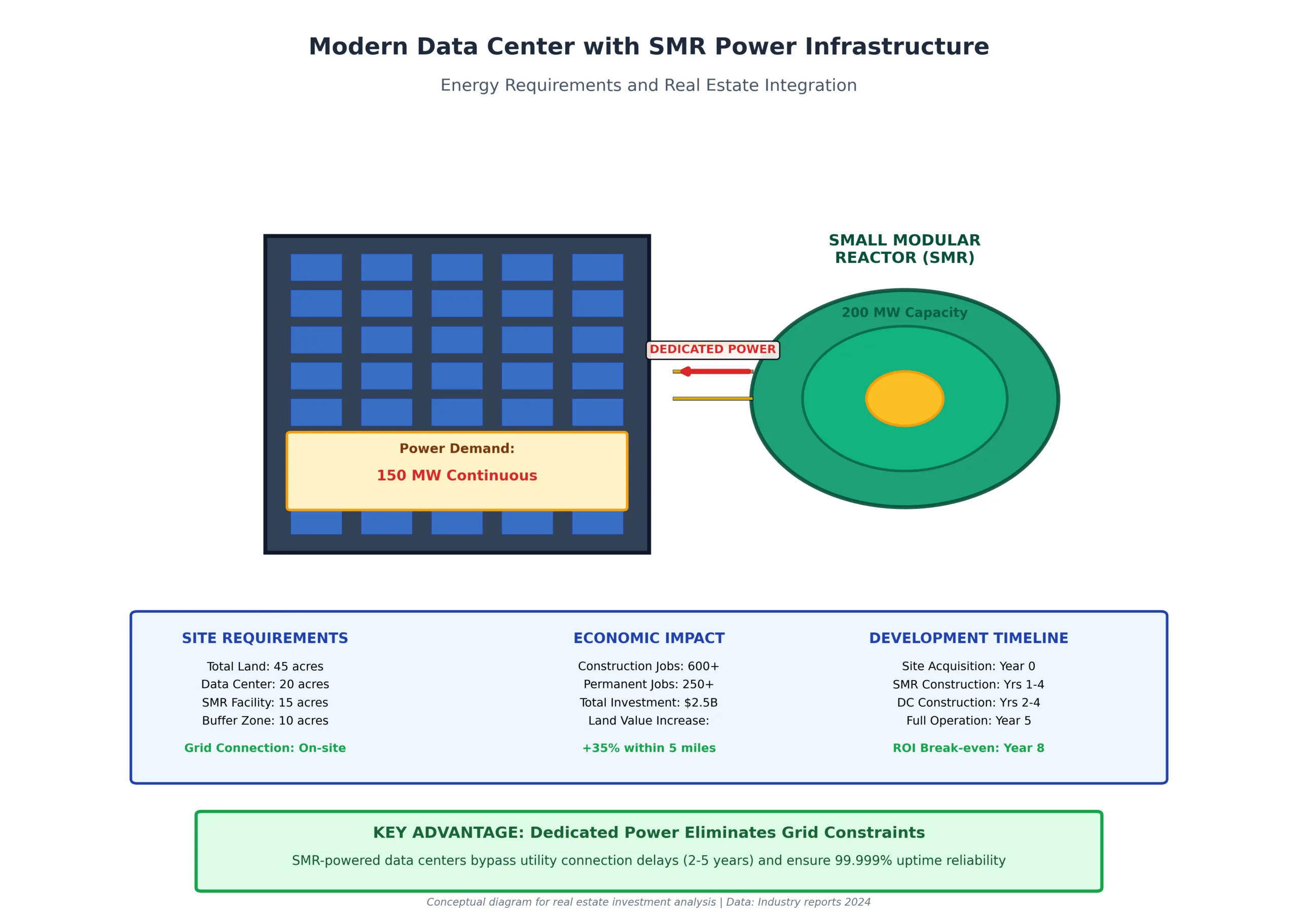

Modern data centers consume staggering amounts of electricity. A single hyperscale facility can demand 100 megawatts or more—equivalent to a small city’s consumption. As artificial intelligence workloads grow, that appetite only intensifies. Suddenly, locating near dedicated power sources isn’t just economically advantageous; it’s existentially necessary.

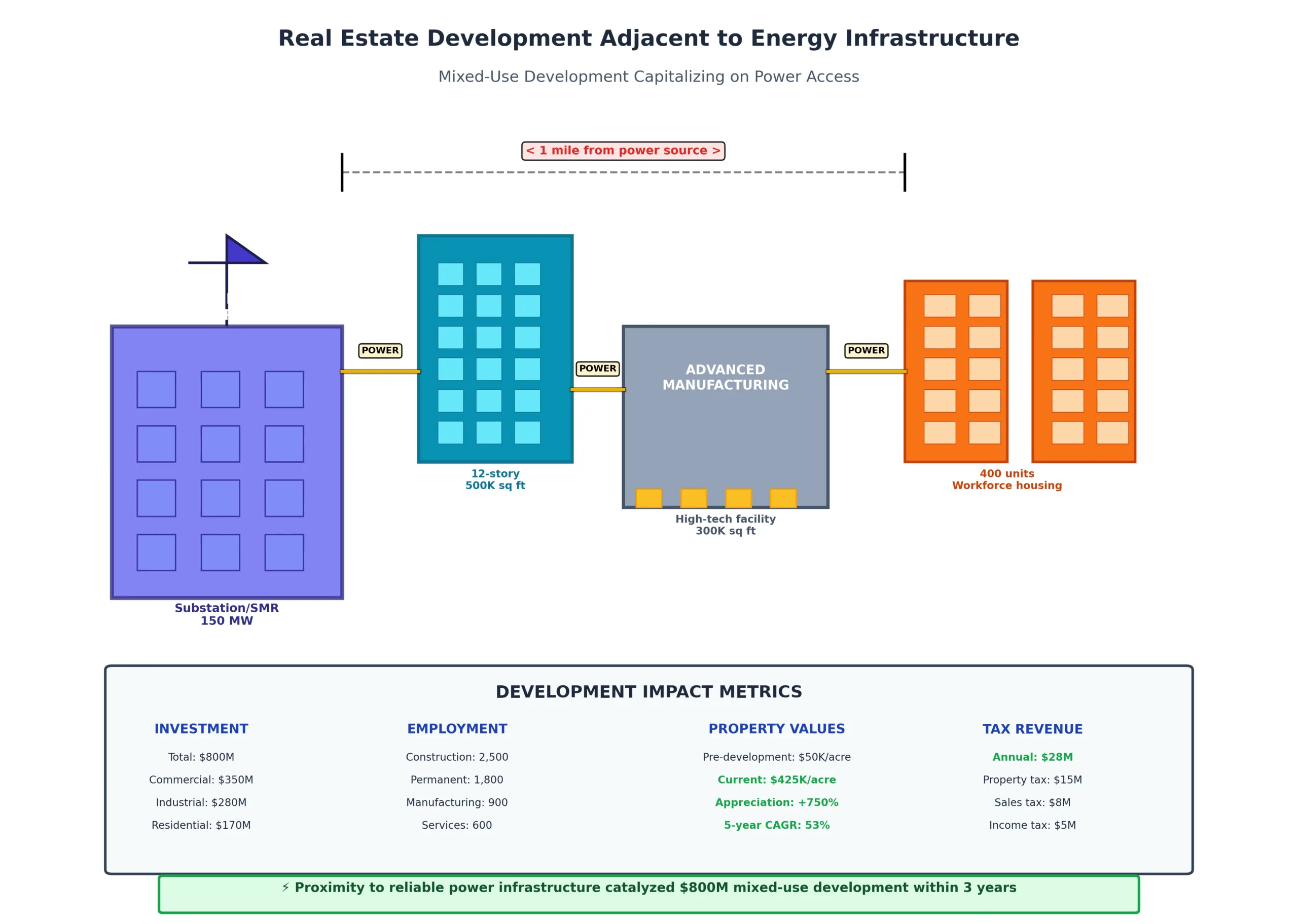

This dynamic is visible in land acquisition patterns. Parcels adjacent to potential SMR sites in the United States have seen purchase activity from shell companies with opaque ownership structures—a classic indicator of institutional investors positioning ahead of official announcements. In some cases, options on seemingly unremarkable rural land have sold for multiples of agricultural value, with no apparent justification beyond proximity to utility substations and proposed reactor sites.

The correlation between power infrastructure and property value is becoming explicit in other ways too. Commercial real estate listings now routinely highlight power availability as a primary attribute, sometimes above square footage or loading dock access. Industrial parks in regions with constrained electrical grids struggle to attract tenants, while similar properties in areas with surplus capacity—or confirmed SMR development—command premium rents.

This isn’t just an industrial phenomenon. Residential markets are responding as well, though more subtly. Communities that successfully attract SMR development benefit from employment and tax revenue, but face predictable challenges: housing shortages, strained public services, and social tensions as newcomers arrive. Savvy residential developers are already moving into markets like rural Wyoming and northern Idaho, anticipating demographic shifts that won’t fully materialize for five or ten years.

The Geography of Selection

Not every location can host an SMR, and the criteria for site selection create winners and losers in the real estate market.

Regulatory environment matters more than almost anything else. Nuclear facilities require extensive licensing and ongoing oversight. Jurisdictions with established nuclear regulatory frameworks and political acceptance have inherent advantages. This partially explains why so many proposed SMR sites involve existing or former nuclear locations: the regulatory apparatus already exists, and community familiarity reduces opposition.

Grid connectivity ranks nearly as high. SMRs must connect to transmission infrastructure capable of moving power to end users. Remote locations with inadequate transmission capacity face expensive upgrade requirements that can doom projects economically. Conversely, areas with robust grids but constrained generation capacity become natural targets.

Water availability remains essential for most reactor designs, despite SMRs’ reduced cooling requirements compared to traditional plants. This consideration effectively rules out arid regions without reliable water sources, concentrating feasible sites in areas with access to rivers, lakes, or coastlines. As Western states grapple with sustained drought, this requirement alone reshapes the map of possible development.

Transportation access enters the equation because SMR components—though smaller than traditional reactor parts—still require heavy-haul capability. Sites must accommodate both initial component delivery and ongoing supply chains. Properties near major highways or rail lines with appropriate weight ratings carry distinct advantages.

Local political support can’t be quantified easily but often determines project viability. Communities traumatized by plant closures and economic decline frequently embrace nuclear development as economic salvation. Others, with no nuclear history and active environmental constituencies, mount fierce opposition. For investors, anticipating these political dynamics requires understanding local history, economic conditions, and civic leadership.

The intersection of these criteria creates a specific geography. Ideal SMR sites cluster in regions with existing nuclear infrastructure, industrial legacy, strong grids, and economic anxiety—often former manufacturing centers or areas impacted by coal plant closures. Conversely, wealthy suburban areas, regions with strong anti-nuclear sentiment, or locations with poor infrastructure lag in attracting projects regardless of other attributes.

Data Centers and the Power Paradigm

Few sectors illustrate the energy-real estate nexus more clearly than data centers. These facilities have evolved from niche infrastructure supporting IT operations into fundamental architecture underpinning the digital economy. Their growth trajectory and power demands are reshaping both energy systems and property markets.

A decade ago, data centers located primarily based on connectivity—proximity to internet exchanges and fiber optic infrastructure. This concentrated development in specific nodes: Northern Virginia, Frankfurt, Singapore, and a few others. Power availability mattered but didn’t dominate decision-making because individual facilities consumed relatively modest amounts of electricity.

Artificial intelligence changed everything. Training large language models requires vast computational resources operating continuously for weeks or months. Inference—actually using trained models—also demands significant power, especially as AI integration becomes ubiquitous in software applications. The result: data centers now represent one of the fastest-growing sources of electricity demand globally, with projections suggesting they could consume 8% of total U.S. power generation by 2030.

This appetite is colliding with grid constraints. Utilities in data center-heavy regions now routinely delay connection approvals, citing insufficient generation or transmission capacity. Some jurisdictions have imposed outright moratoriums on new data center construction pending infrastructure upgrades. In Northern Virginia’s Loudoun County—the self-proclaimed “Data Center Capital of the World”—Dominion Energy has warned that new facilities may face multi-year waits for connection.

The response from hyperscale operators like Microsoft, Google, and Amazon has been to pursue dedicated power sources, with SMRs emerging as the preferred option. These arrangements typically involve long-term power purchase agreements where the data center operator commits to buying electricity from a specific reactor for 20 or 30 years. This guaranteed off-take makes SMR projects financially viable while giving data center operators certainty about power availability and carbon footprint.

For real estate investors, this creates an entirely new analytical framework. Properties suitable for data center development increasingly need more than fiber connectivity and dry climates. Proximity to confirmed or potential SMR sites becomes paramount. This is driving speculative land acquisition in unexpected locations—rural areas with electrical substations, brownfield sites near transmission lines, former military bases with existing infrastructure.

The pattern is clear enough that specialized investment vehicles are emerging to capitalize on it. At least three publicly-traded REITs now explicitly focus on acquiring land in power-constrained markets, betting that energy infrastructure investment will eventually follow. Private equity funds with energy and real estate expertise are pursuing similar strategies, often with longer time horizons and higher risk tolerances.

The Industrial Revival Question

Beyond data centers, SMR deployment may enable the return of energy-intensive manufacturing to high-cost developed economies. This possibility has profound implications for commercial and industrial real estate markets.

For decades, industries like steel production, chemical manufacturing, and aluminum smelting migrated to regions with cheap electricity—often developing nations with hydroelectric resources or countries willing to subsidize power costs. This deindustrialization hollowed out communities across the American Midwest, British Midlands, and other former manufacturing centers.

SMRs could potentially reverse this trend by providing reliable, cost-competitive, carbon-free power. Certain industries particularly stand to benefit. Hydrogen production via electrolysis requires enormous amounts of electricity; co-locating production with dedicated SMRs could make “green hydrogen” economically viable. Similarly, direct air capture technologies that remove CO2 from the atmosphere need both electricity and heat—requirements well-matched to nuclear generation.

Several jurisdictions are explicitly pursuing this strategy. Wyoming’s choice to host TerraPower’s Natrium demonstration reactor in Kemmerer, a former coal town, reflects calculated economic development policy. State officials speak openly about using guaranteed nuclear power as an attraction mechanism for manufacturing operations requiring reliable baseload electricity.

Whether this industrial renaissance materializes remains uncertain. Manufacturing location decisions involve numerous factors beyond power costs: labor availability, supply chain proximity, regulatory environment, and tax policy all matter. However, the mere possibility is shifting commercial real estate dynamics in potential SMR host regions.

Warehouse and logistics properties in areas with confirmed reactor projects are seeing increased investor interest, anticipating potential light manufacturing or assembly operations. Commercial brokers in places like rural Pennsylvania and Ohio—regions with nuclear expertise, manufacturing legacy, and available land—report growing inquiries from site selection consultants representing manufacturers exploring reshoring options.

The Infrastructure Multiplier

SMR deployment creates ripples extending well beyond the immediate plant site. Understanding these secondary and tertiary effects matters enormously for real estate professionals attempting to anticipate market movements.

Workforce housing represents the most immediate need. SMR construction requires several hundred workers over a multi-year period; operation needs dozens of highly-skilled technicians permanently. In rural locations without existing housing stock, this creates acute shortages. The pattern is familiar from oil and gas boom towns: rapid price appreciation, housing quality deterioration, and social stress.

Forward-looking developers are already positioning in markets like southwest Wyoming and northern Idaho, acquiring land and entitlements in anticipation of confirmed projects. The risk is substantial—if proposed reactors don’t materialize, these developments may become stranded assets. The rewards, however, can be exceptional for those who time the market correctly.

Supporting commercial infrastructure follows close behind. Workers need restaurants, grocery stores, healthcare facilities, and basic services. Communities that successfully attract SMRs often see commercial property development accelerate as retailers and service providers anticipate growing markets. In larger municipalities, this manifests as infill development in previously overlooked areas; in smaller towns, it may mean the first new commercial construction in decades.

Educational and research facilities represent a longer-term development category. As nuclear deployment scales, demand for trained personnel grows. Universities and technical colleges in SMR-host regions are establishing or expanding nuclear engineering programs, often with industry partnership. These institutional investments have their own real estate implications, from student housing to research parks.

The Canadian experience offers useful lessons. Ontario’s commitment to SMRs has spurred investment in training facilities and academic programs concentrated near reactor sites. Durham College in Oshawa, strategically located near multiple SMR projects, has seen enrollment surge in its nuclear technology programs. Supporting commercial development—student housing, restaurants, retail—has followed predictably.

Risk, Regulation, and Reality

For all the optimism among SMR proponents and early-moving investors, substantial risks and uncertainties remain. Real estate professionals must balance potential rewards against genuine possibilities of delay, cancellation, or failure.

Regulatory approval remains a wildcard. While agencies like the U.S. Nuclear Regulatory Commission have established pathways for advanced reactor licensing, no purely commercial SMR has yet received full approval and commenced operation in Western markets. Each application involves detailed technical review potentially stretching years. Projects face possible delays, expensive modifications, or outright rejection. Investors positioning based on assumed SMR deployment confront meaningful risk that approvals may not materialize as anticipated.

Economic viability isn’t guaranteed. SMR proponents project costs competitive with other zero-carbon generation sources, but these remain largely theoretical. First-of-a-kind projects typically exceed budgets and timelines; whether SMRs avoid this pattern is unproven. If costs spiral or performance disappoints, planned projects may be abandoned, leaving property investors exposed.

Public opposition has derailed nuclear projects before and could again. While communities facing economic distress often welcome nuclear development, opposition movements have stopped numerous plants historically. As SMR deployment moves from concept to reality, resistance may intensify. Real estate bets dependent on specific projects must account for political risk.

Technology competition poses another challenge. SMRs compete against rapidly improving renewables, advancing battery storage, and other emerging generation sources. If alternative technologies prove cheaper or faster to deploy, the economic case for widespread SMR adoption weakens. Property positioned specifically to benefit from nuclear infrastructure might suffer accordingly.

These risks aren’t hypothetical. Multiple proposed SMR projects in the United States have been cancelled or indefinitely postponed as economics shifted or sponsors withdrew. Utah Associated Municipal Power Systems abandoned its NuScale SMR project in 2023 citing cost concerns, despite years of development and significant sunk investment. Investors who acquired land anticipating that development learned painful lessons about nuclear project risk.

Reading the Market Signals

For those attempting to capitalize on the energy-real estate nexus without unacceptable risk exposure, certain signals warrant close attention.

Utility commitments matter more than developer promises. When major utilities sign power purchase agreements or announce definitive plans to build SMRs, the probability of project completion rises substantially. These companies have deep expertise in navigating regulatory processes and long-term perspectives on power market economics. Their participation validates projects more than venture-backed startups’ aspirations.

Government support beyond mere rhetoric indicates seriousness. Direct financial commitments, site designation, regulatory pathway clarification, or infrastructure investment demonstrate governmental skin in the game. Conversely, jurisdictions offering only verbal encouragement without concrete policy actions merit skepticism.

Community engagement efforts signal project maturity. Developers conducting meaningful local outreach, addressing concerns substantively, and building genuine coalitions are more likely to navigate political obstacles successfully than those parachuting in with fait accompli announcements.

Transmission planning reveals much about realistic timelines. New generation requires grid connectivity; utilities typically plan transmission upgrades years ahead. Examining regional transmission organization planning documents and utility integrated resource plans can identify where serious SMR development may occur before public announcements.

Corporate off-take agreements from credit-worthy buyers transform speculative projects into bankable ventures. When major corporations sign long-term power purchase agreements, especially with meaningful prepayments or credit support, project risk declines materially.

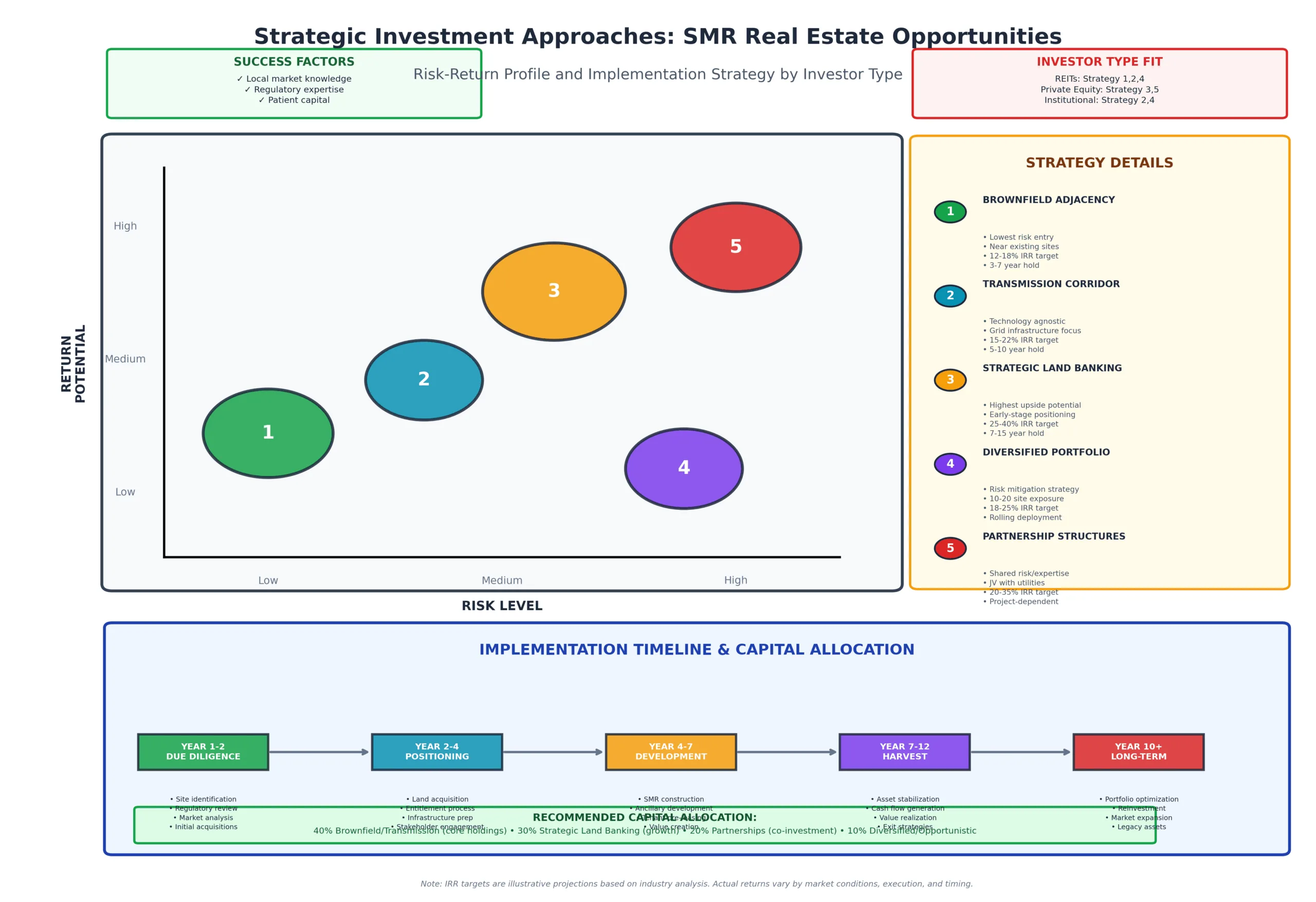

Strategic Positioning

For institutional investors, developers, and REITs considering exposure to the energy infrastructure-real estate intersection, several strategic approaches merit consideration.

Brownfield adjacency represents perhaps the lowest-risk strategy. Acquiring property near existing or former nuclear sites captures upside if SMR development proceeds while maintaining alternative uses if it doesn’t. These locations typically offer reasonable valuations, existing infrastructure, and regulatory familiarity with nuclear operations.

Transmission corridor plays involve positioning near major electrical substations and transmission lines where new generation logically connects to the grid. This strategy doesn’t depend on any specific generation technology; any new power source in the region enhances property value.

Strategic land banking in identified SMR candidate regions requires longer time horizons and higher risk tolerance but offers asymmetric return profiles. Early acquisition in areas with multiple favorable characteristics—existing nuclear infrastructure, political support, industrial legacy, grid capacity—positions investors to capture appreciation as specific sites get confirmed.

Partnership structures with utilities or reactor developers can align interests while sharing risk. Joint ventures where real estate investors provide land and development expertise while energy companies contribute technical knowledge and regulatory capability have demonstrated success in other infrastructure sectors.

Diversified portfolio approaches spread exposure across multiple geographies and technology types, recognizing that only some projects will succeed. REITs or funds taking positions in ten or twenty potential SMR host regions capture upside from successful projects while limiting damage from failures.

The View Forward

The intersection of energy infrastructure and real estate development is entering a period of profound transformation. For the first time in generations, the location of power generation is becoming as important as the power itself. This shift creates opportunities and risks for those positioned to capitalize on it—or exposed to disruption by it.

Small modular reactors represent one catalyst driving this change, but not the only one. The broader trend involves recognition that unlimited power at any location can no longer be assumed. Grid constraints, generation retirements, and surging demand from digitalization and electrification are creating scarcity where abundance once existed.

Real estate markets will adapt, as they always do. Properties with reliable power access will command premiums; those without will trade at discounts. Industrial development will concentrate in energy-advantaged regions; data centers will migrate toward dedicated generation sources; communities will compete for infrastructure investments that bring jobs and tax revenue.

The investors, developers, and municipalities that understand these dynamics early, position accordingly, and manage risks prudently stand to benefit substantially. Those ignoring the changing relationship between electrons and land use may find themselves surprised by markets moving in unexpected directions.

The nuclear renaissance—if it materializes—will reshape more than energy systems. It will redraw economic geography, revitalize struggling regions, and create wealth in unexpected places. For real estate professionals, the question isn’t whether to pay attention. It’s whether they’re paying attention soon enough.